Whether we don’t mind having debt or it gives us anxiety, most of us carry some percentage of it in our balance sheets. One of the most common questions clients ask me, is whether they should pay down their debt or invest the extra money in the market. Most of us carry some percentage of debt in our balance sheets. Some of us don’t mind having debt. For others, it’s a cause for anxiety.

It’s important to note these decisions are personal and your comfort level is most important. So, whatever your end results are, commit to the decision that will provide you with peace of mind.

What do you need?

The Debt Side:

- Highest interest on debt carried: It can be your mortgage, Equity line of credit, business loan, or credit card debt.

- Debt account type: Certain debt has tax advantages. For example, mortgage payments on your primary home, and payments on student loan debt. Credit card debt however doesn’t.

- Is the interest on your debt tax deductible? This matters because any part of the interest that is deductible will lower the rate you are paying, it makes your debt cheaper to carry.

The Investment Side:

- Expected rate of return: One of the most important parts of this number is to remember returns are not guaranteed, and when you are measuring this number you need to remember this number can be lower/higher than expectations or even negative.

- Investment account type: Same as above, certain accounts have tax advantages. For example, if you are investing your money in a tax-free account like a Roth IRA, then the return you receive will generally not be subject to taxation. But if it’s a tax-deferred account, you will pay income taxes on the return. If it’s an individual or a joint account then you will pay capital gains on the account.

- Is the interest on the return taxable? This matters because any part of the return you pay taxes on will lower the actual rate of return you are receiving.

May Need on Both Sides

Tax Bracket: For the purposes of the analysis, the marginal tax bracket is used to measure the deductibility and taxability of the interest rate and to find the capital gains tax rates when applicable.

How it works…

Debt:

Non-Deductible rate: = Stated rate

Deductible debt rate: Interest rate x (1-Marginal Tax Bracket) = Reduced rate in debt

Investment:

Non- Taxable rate = Stated rate

Taxable rate = Expected rate of return x (1-Marginal Tax Bracket or Capital gains tax rate) = Reduced rate in investment

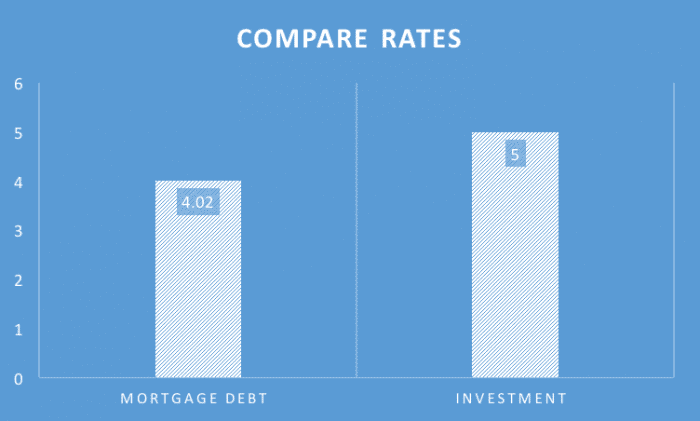

Case example

You have a mortgage loan on your primary home with an interest rate of 6%. The interest is tax deductible. Tax bracket is 33%. You can pay down your mortgage or you can invest the money in your Roth IRA and your expected rate of return on investments is 5%. The interest is not taxable.

Example:

Debt: 6% (1-.33) = 4.02%

Investment: 5%

The hypothetical investment results are for illustrative purposes only and should not be deemed a representation of past or future results. Actual investment results may be more or less than those shown. This does not represent any specific product [and/or service].

In this case although at first glance it seems the interest rate in the mortgage loan is higher; when we compare the rate paid after adjusting for taxes vs. the expected rate of return after not having to adjust for taxes, then it makes more sense to invest the money on the Roth IRA than to pay down the mortgage. Not all cases are this simple, and as you can see there are many factors which can affect a financial situation.

Money is personal, which is why it’s important to work with someone who understands your personal goals and objectives. If you are personally debt averse, your trusted advisor can help you make the right decision for you. With the help of this simple analysis, you can feel confident you are making an informed decision when it comes to your finances.